One-year vesting schedules are probably a raw deal for employees

If you haven’t subscribed yet, you can get thoughts and musings about personal finance and whatever else I find interesting straight to your inbox by clicking here:

I happened across an interesting article recently from The Information (paywall ahead, unfortunately), about how Stripe and Lyft are changing their equity vesting schedules to one year. If you’ve had any experience with stock options (or read my previous posts on the subject), you’re probably familiar with the fact that most companies offer equity in option grants that vest over four years, with a one-year vesting cliff (leave before one year, and you walk away with nothing). At face value, getting all your equity after one year sounds like a game changer. But is it really?

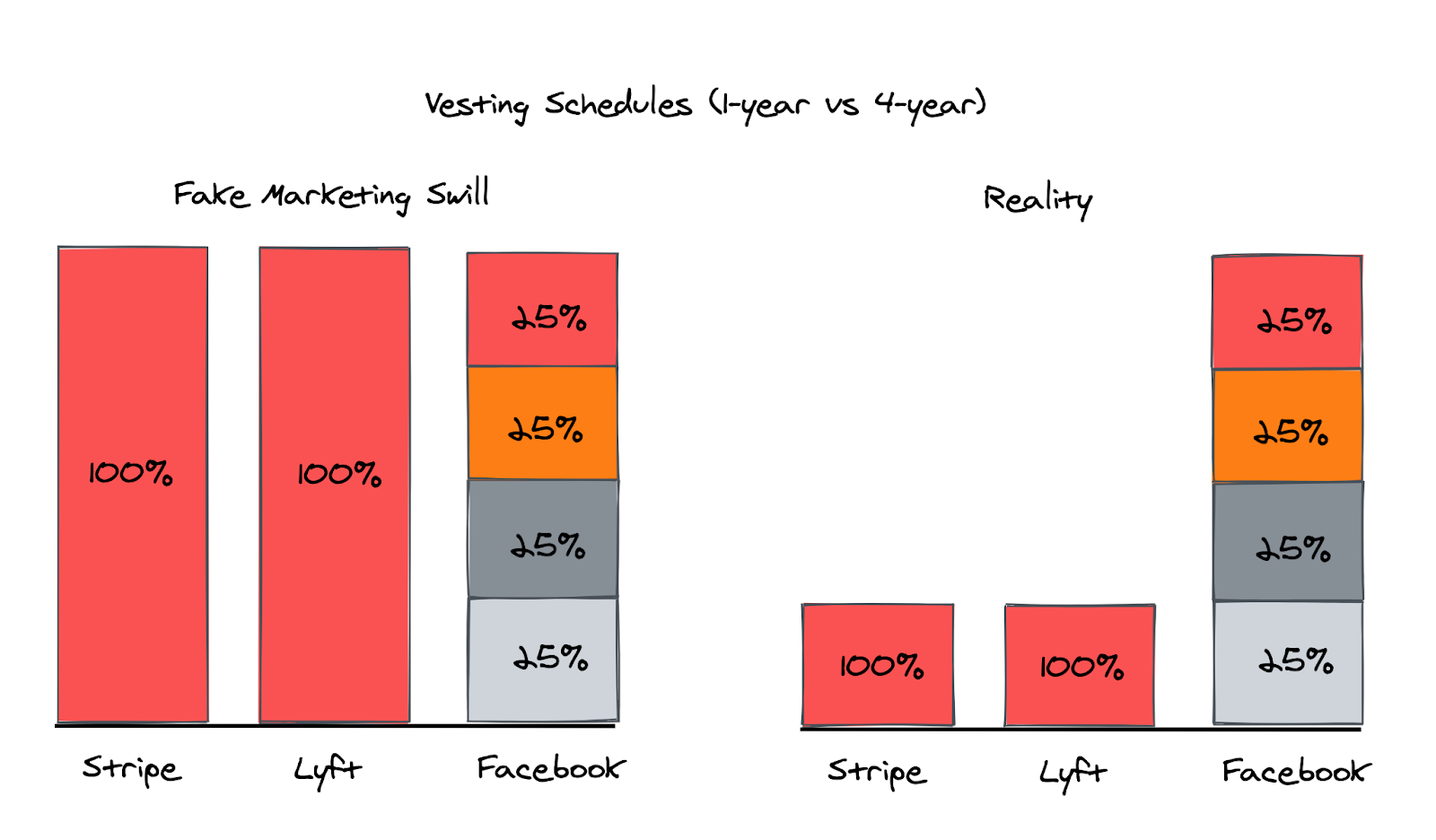

The reality of the situation is that this article is probably a marketing bonanza for Stripe and Lyft’s recruiting teams. There’s a really infuriating graphic in the original article that looks along the lines of this chart on the left:

What drives me nuts here is that it paints the idea that these one-year grants are the same size as the four-year grants that employees would otherwise get at companies with a standard vest. Now, I haven’t seen the volume of these option/RSU grants, so maybe they really are the same size as a four-year grant, and maybe you’ll call me a haggard cynic here, but I’m pretty damn sure the left picture is some fake news, and the right picture represents a version of reality that is much closer to the truth. (If you have a one-year vest, and can refute my assertion here, I want to hear from you!)

The situation is probably a much better deal for the company than it is for the employee, but let’s walk through this a bit to understand the situation better. Let’s say a company is making you an offer, and offers a package that includes $50,000 of equity per year (calculated based on the preferred price, for clarity) for four years, so $200,000 total. A couple of things happen here:

All your options will be locked in at the current strike price, which is likely lower than whatever the strike price is going to be four years from now.

You’re being allocated $200,000 of options in a cheaper company than it is likely to be four years from now.

I’m kind of saying the same thing two different ways, but let’s make the scenario a bit more real.

Scenario 1: Four-Year Vest

Let’s consider a company with the following financial picture:

Series B company, just fundraised at a $100M post-money valuation

20M outstanding shares (which means the investors paid $5/share)

FMV is 50% of the post-money valuation (so $50M, which is what determines the strike price, and this implies that the strike price is $2.50)

The company wants to make you an offer (yay!). They offer you an options package that they value at $200,000 (which is to say, the options are worth $200K at the preferred price of $5, which implies that you’re getting 40K options). This package represents about .2% of the company, and the strike price will be $2.50.

If you stay at the company for four years, we’ll assume you see:

Two additional funding rounds

20% dilution in each round

2x valuation step-ups in each funding round

FMV is 50% of the post-money valuation after each round

This is a pretty darn good situation for most folks, because at the end of it, you own .128% of a $400M company, and your equity that you’ve vested over the four years is now worth $512K instead of $200K, and you pay $100K to exercise, so end up with a net outcome of $412K before taxes. Sweet!

Scenario 2: One-Year Vest

Now let’s look at this with one-year vests. If you think you’re going to get $200K upfront in one year, you’ve probably got another thing coming. Almost assuredly, the way this ends up working out is that the company is going to give you ¼ of the amount of equity, and just give you annual grants each year.

Assuming the same scenario as above, let’s get a little more granular with the funding rounds, and say that they occur at 18 months into your tenure, and then again at 36 months, before you finish the equivalent amount of vesting at 48 months. This is going to get a little more complex, but let’s see if we can work through it (I’m being bad here, and not quite showing how I’m calculating all the numbers, but I’ve given you all the assumptions necessary to recreate how I’ve calculated this, so that replicating the analysis can be an exercise for the reader, if you don’t believe me). In this scenario, you receive:

$50,000 in month 1, at a $100M valuation (.05% or 10K options, $2.50 strike price)

$50,000 in month 12, still at a $100M valuation (since the first funding round happens at 18 months) (another .05%, another 10K options, still $2.50 strike price)

$50,000 in month 24, now at a $200M valuation (.025% this time, represented by 6K options, and strike price on this has increased to $4.17)

$50,000 in month 36, which happens to coincide with the last funding round, so we’ll assume you get the strike price after the round, which means the company is now worth $400M (.0125%, represented by 3600 options this time, at a $6.94 strike price)

If we start extrapolating all of this out, our grants, at the end of all this, are worth:

Grant 1: 10,000 options, costs $25K to exercise, and is worth $138K

Grant 2: 10,000 options, costs $25K to exercise, and is worth $138K

Grant 3: 6,000 options, costs $25K to exercise, and is worth $83K

Grant 4: 3,600 options, costs $25K to exercise, and is worth $50K

The total cost to exercise is still $100K, but the four years of equity is only worth $409K, so your net here is only $309K, compared to the $412K (a 25% difference!) that you made if you’d gotten a four-year grant at the start of the job. Suddenly, this situation doesn’t look so awesome. Parts of this scenario are also a bit more optimistic than reality would likely be. For example, FMVs and strike prices will tend to get closer to the preferred price as the company matures, so assuming that the strike price is 50% of the preferred price might be true in one round, but probably not all three. This would result in higher strike prices for employees in later rounds, which erodes even more of the value of the options in the one-year vest case. The even sadder part is that for the buzziest private companies, the situation is much worse. Valuation step-ups can be anywhere from 3-5x, and some companies are raising a round per year.

But does this ever make sense?

In the case of public companies, where valuations might fluctuate wildly, especially soon after IPO, and valuations tend not to just go up, you could argue that there is some value in this type of vest. If you happen to join on a day when the stock price is high, you could get burned with a four-year vest, and it’s possible to craft a scenario where you come out on top with one-year vesting cycles. However, I’d argue that this is the whole reason that Employee Stock Purchase Plans (ESPPs) exist. Now ESPPs aren’t quite the same as options or RSUs, because you have to buy them at market prices, and stock that you purchase through an ESPP doesn’t vest or just get given to you. However, it does allow (usually public company) employees to purchase stock over time, and almost always at discounts to the current market value.

Why does the company care about these things?

I’m not a CFO or a VP, Finance, but I’ll share my perspective on the psychology of companies. The short answer to this question is that I believe most companies prefer to give away cash rather than equity. A dollar is a dollar today and a year from now, and while there might be some nightmare inflationary world ahead of us, the dollar’s value isn’t going to change super dramatically over the course of four years. Stock, on the other hand, especially in today’s market climates, can be worth a huge amount more tomorrow, and so companies have a strong incentive to give away as little as possible to employees today, so that they can give away less stock tomorrow, and still be providing the same economic value. There are also other types of purchases, namely acquisitions, that companies would generally rather use stock for (especially private companies). Companies with high stock prices, for example, would strongly prefer to use stock as the primary mechanism for making acquisitions, because it allows them to give away something that has a) large perceived economic value and b) it can’t be used for paying day-to-day bills. If they give away less stock to employees as they hire them and retain them, they have more stock to be parceled out for these larger stock-based purchases.

The moral of the story here is that there are a lot of different angles for why a company might prefer a one-year vesting schedule to a four-year vesting schedule, and for employees, it might seem alluring to vest everything in year one, rather than having to wait four years to earn your due. The thing to watch out for is how big that one-year vested grant really is, and what the company plans to do to refresh your grant after that one year is up. Do your homework, evaluate the value of the offer, and if it all adds up, awesome, take the job! Just make sure you know what you’re getting yourself into.