The Multiples are Falling!

Hey folks, I don’t know if you’ve heard, but apparently the tech sector’s been having, like, a rough go of it lately. And if you’ve been paying any attention at all to the tech business world over the last 6 months or so, you’ve probably come across the term “multiple compression,” which is finance jargon for “we’re having a bad time.” It’s been a major factor in the dwindling valuations of large tech companies, both public and private, and the entire market is going to have to face the music sooner or later. On the bright side, in some ways, this actually signals a return to rationality in valuations, which we’ve sort of been ignoring for a little while.

If you don’t know what I mean when I reference a multiple, it’s a way of valuing a business, and it actually represents a ratio. Depending on your exact valuation approach, this ratio might be the price of a stock to the earnings or profit that the stock generates (P/E - price-to-earnings ratio). In the private company world, where I live, profit is still a mythical oasis of financial prudence, so there’s not really any earnings to speak of. In this world, the type of multiple that is typically used is based on revenue, either the revenue generated by the company in the last twelve months (LTM or “backward”) or the revenue that the company expects to generate in the next twelve months (NTM or “forward”). More explicitly, the ratio is between the company’s market capitalization (its valuation), and the NTM or LTM revenue.

The beauty of this multiple-based valuation system is that it makes it really easy for someone to look at financial results for a company, and determine what that company is worth, and what price they should be willing to pay for the stock. If a company is worth $100M today, and generated $10M of revenue last year, the implied LTM multiple is 10x, and if I think that the company is going to make $25M at the end of next year, I might be willing to pay a share price that values the company at $250M. At the end of the day, I’m really paying to own a piece of future cash flows that the business generates.

So with this in mind, what people mean when they say “multiple compression” is that the multiple used to value a company is getting smaller. The business may keep growing, but the stock price is staying the same, or going down. Cool cool cool, that’s fun. You might ask: what the heck is causing this multiple compression?

Right now, in the end, a lot of it comes down to macroeconomics. Inflation is high, because we’ve been in a low-interest environment for a long time, and the worlds’ governments pumped huge amounts of cash into the economy in order to keep it moving through the pandemic and beyond, which increases propensity to spend, which in turn drives up demand and costs of goods and services, which, if left unchecked in the long term, is bad. So the Fed steps in and starts jacking up interest rates, as they are wont to do, because as interest rates rise, it gets more expensive to borrow money, and instead of spending, people save. Demand falls, which causes prices to drop to balance the supply/demand curve, and inflation goes down. The problem we’ve got right now is that trying to raise rates just enough, without crashing the economy and plunging ourselves into a global recession, is…challenging. If you’ve ever played the notoriously hard Dark Souls games, and you’re like me, and terrible at playing Dark Souls games, it’s kind of like that, but if there was a nightmare mode.

In the venture markets, there’s still a huge amount of committed capital that’s been raised for funds, so while it’s going to be deployed, LPs are seeing their broader portfolios drop, which in turn raises scrutiny on investment committees, and the focus on delivering good returns, which drives VCs to rush to invest in the teeny-tiny subset of companies that are still growing at a fast clip and have good efficiency metrics to boot, instead of the spray-and-pray approach we’ve seen in the last several years. So we arrive at multiple compression.

If you work for a private company, identifying the multiple that investors would apply to your company can be difficult. A core concept used in public marketplaces is the idea of comparables. While Confluent and HashiCorp develop very different products, they both monetize open-source software, and generate revenue from either providing support for on-premise versions of their software, or from their cloud-based PaaS offerings, and they generally sell to similar buyers (usually the CIO). This kind of comparison leads investors to use similar metrics and KPIs to value these businesses, and so often larger market trends will impact comparable businesses in similar ways. (This, for that, you know? It’s like DoorDash, but for developer infrastructure). For private companies, it can be a little bit harder, since private companies are usually earlier on in their lives, and often also have price premiums due to growth potential, but you can often use public company multiples as a guide for what private company multiples might look like.

If you want to learn a lot more about how SaaS businesses are being impacted by the multiple compression trend, consider this my strong plug to check out Jamin Ball’s Clouded Judgement newsletter. He does a great job of dissecting the market and examining impacts, and below you can see a stolen chart (I’m not sorry, it’s a really useful chart):

This looks at Enterprise Value (a company’s valuation or market capitalization) ratio to their forward revenue. It’s quite clear to see that for the top 5 SaaS business peaked in the January 2022 timeframe, around an 80x forward multiple (meaning if your business is expecting to generate $10M this coming year, your business is worth $800M), and then by late October, has dropped to 15.4x (implying that that same business is no longer worth $800M, but in fact only worth $154M). That is a big drop.

As a startup employee, you may be wondering: what the hell does this have to do with me? Well, most acutely, it means that if you joined a startup that raised money at any time in 2021 or prior to, let’s say, March 2022, your company is not worth whatever investors said it was worth at the time of the last raise. And I’m here to tell you that that’s probably ok. It’s not great, obviously, but it may not be the end of the world. However, it does have a ton of implications about how you need to be educating yourself, and thinking about the value of your equity.

How fucked are we (the royal, corporate we)?

By raising at sky-high valuations, with multiples dropping like it’s hot, companies set themselves up for extreme expectations when they need to raise their next round. Let’s come back to this $10M ARR company. If it’s now got a 15.4x forward multiple, this means that they will be back at the $800M valuation when their NTM revenue is projected to be about $50M. The company needs to 5x their revenue in order to get back to the valuation they just raised at, and if they fundraised with that revenue projection, that would likely end up being a flat fundraising round. Not an up-round. No one increases their stock value, do not pass go, go straight to jail.

Of course, you’re sitting there thinking “oh yeah, but my company is a rocketship, and we will be at that revenue target next year,” and no, you’re almost certainly wrong. The standard 5-to-7-year IPO trajectory starts with tripling revenue in your first couple years of monetization, and doubling in the next three years. If you are a top-tier, number one startup, and you are actually on that trajectory (and assuming a potentially-imminent recession doesn’t knock you off course), you probably do something $2M → $6M → $18M → $36M → $72M. Or maybe you’re even more awesome, and you go $3M → $9M → $27M → $52M. Each of those trajectories still ends with your company needing 2 years to grow into the valuation, and then a third to get to a point where you can raise an upround with clean terms.

Clean terms? Let’s clarify. Investors buy preferred stock. Employees buy common stock. Investors who buy preferred stock get a whole bunch of additional bells and whistles – board seats, information rights, liquidation preferences, pro rata rights, etc. In the forever-bull-market of 2021 and earlier, as an employee, you didn’t really need to know about many of these things, because investors were racing to stash money in every startup they could find: you have a deck, and an engineer? Have some cash! Diligence was not really a thing that was rigorously done in late 2021.

A key thing to be aware of is that most companies raise money on 18-24 month timelines. They have a business plan, and they share it with prospective investors, and the investors say “yes, yes, this is a good plan, here is some money.” Then when 12-18 months have passed, the investors come back and say “You must be getting close to needing more money! We have just the thing for you!” But, oh no! Even if we triple, and double, and double, it’ll still take us three years to grow into our valuation, and we don’t have three years of capital! We need more money now! And so the investors look at your financials (because now that the market is back to sanity, we do diligence again), and they say “Oh no, this is bad, very bad, but we care about you, and we’re your partner in this! So we’ll make you a deal: you can keep your valuation stable, but we’re going to need guarantees about our returns on the capital we invest.” Your partner informs you that they will need to be guaranteed at least a 2x return on their investment.

Liquidation preferences

That guarantee is called a liquidation preference. In reality, this term is always in the funding details, but if you have a clean term sheet, it probably has a 1x liquidation preference. What this actually means is that if the company were to underperform, and be worth less than what the investor paid, the investor gets their money back in full, before any of the other shareholders get paid out. In contract parlance, the term of art is seniority. Preferred stock is senior to common stock, so preferred stockholders get paid back before the more junior common stock. You can probably guess what a 2x or 3x liquidation preference implies, then. The nice thing about a 1x preference is that the only situation in which the investor actually invokes this term is if the company ends up being worth less than the price they paid. But if they have a 2x or 3x multiple, the company actually has to accrue significant value in order to get to a point where the investor will not invoke the preferential treatment. Let’s work through an example!

Let’s say you’re a company valued at $100M, and an investor gives you $30M in exchange for 15% of the company and a 2x liquidation preference. The post-money value of the company is $200M (implied by the amount of stock being purchased, and the price being paid). Let’s say, for ease, there are 10M outstanding shares after the fundraise, so the preferred share price is $20, and the investor owns 1.5M shares. But because the investor has a 2x multiple in here, their stock needs to be worth $60M before anybody else gets paid out, which means the breakeven for employees is now at $400M (which is the valuation at which the 15% that the investor owns is worth $60M). Now, if the company gets acquired for $400M, the investor gets their $60M, and the employees get paid out on the remaining $340M at a price of $40/share, which conveniently lines up with that $400M acquisition price. But let’s see what happens if the company doesn’t make it to $400M. If the company sells at $350M, the investor, with their 2x preference, still gets their $60M, but that now leaves only $290M to go around to the remaining 85% ownership of the company. Which nets a $34.11/share price. Which means the company, for the employees, is paying them out at a rate that implies it was worth $341M. Which is not equal to $400M (I am confident of this, because I have a bachelor's degree in mathematics).

If you end up in this position, as an employee, you are probably first seeing the news that your company was acquired for $350M and are saying “YES! This is awesome!” and then you see the amount that you get paid out, and you are saying “WHAT? No! Expletive!”

And that is how liquidation preferences work.

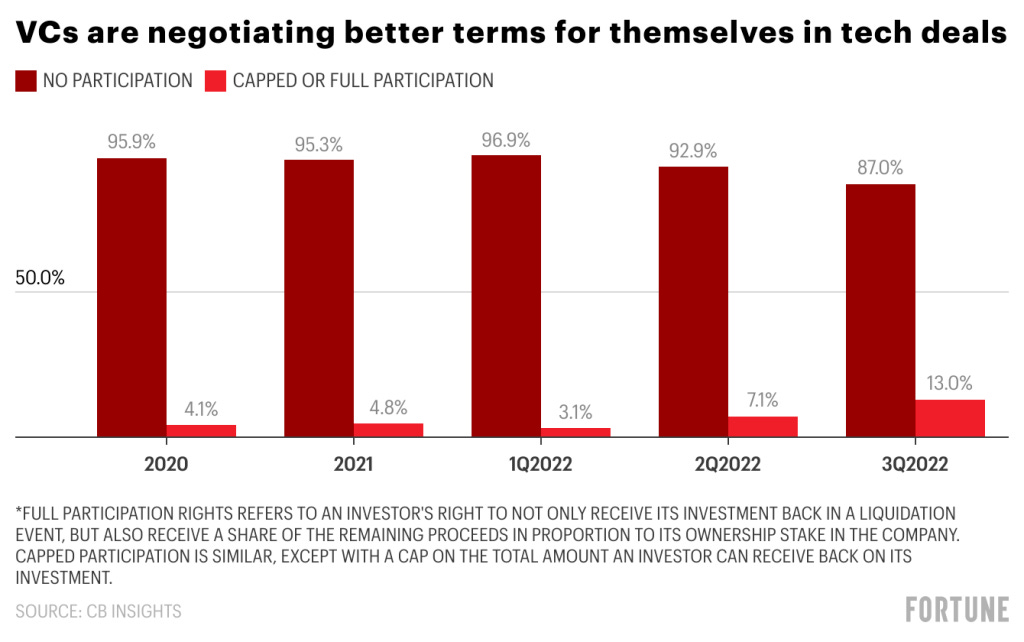

And, indeed, this is actually what’s happening:

That rising 13% of deals with capped or full participation? Those are VCs negotiating liquidation preferences for their funds. Non-participating stock is stock that gets paid out alongside everybody else, effectively putting everybody on an even playing field. Participating stock honors seniority, and participating shareholders get to recoup their investment and then also get some of the cut of the rest of the deal as well. Participation is basically contract-lawyer-legalese for “we get paid before all you chumps.”

How fucked are you (the specific, individual you)?

The short answer, if I’m being totally honest with you, is: you might be fucked. Or you might not. The employees of Good Technology fell into that you-might-be-fucked bucket. Unfortunately, it’s a little difficult to know, and the best thing you can do is to understand all of the dynamics at play. Part of the challenge is that many companies are not likely to be particularly forthcoming about these nitty-gritty terms during job offer discussions, or even with their employees during a fundraising round. If you’re lucky, you work for a company that is fairly transparent, or has a strong enough track record that they haven’t had a need to raise under less company-and-employee-friendly terms. I would certainly encourage people to ask questions like:

“Have we ever raised a round that included liquidation preferences greater than 1x?”

“What is the total dollar value of outstanding participating preferred stock?”

These are good questions to know to ask, but again, your mileage may vary in terms of answers you get. There are also some potential related questions that you might have a better shot at getting straight answers, which can help you suss out the answer:

“How much months of runway did we remaining have when we raised our last round?”

Somewhere in the range of six to nine months would probably be a fairly standard answer to that question. Anything above nine months would feel like a pretty safe situation, where the round was a little bit more opportunistic. Anything under six months, and you’re in a serious danger zone, where the company was probably getting to desperation mode, and might be more willing to compromise on terms. Frankly, if your company didn’t raise money in 2021 or the very early months of 2022, the fundraises to-date might have been relatively clean, but the next one is probably going to be a little less squeaky clean.

Doom and gloom aside, and while our example around liquidation preferences shows the danger to the employee’s stock value that is posed by the specter of unfavorable terms in future fundraising rounds, I ignored the fact that the price for common stock and preferred stock is never actually the same.

Investors pay higher prices for preferred stock because of all those bells and whistles. Common stock typically costs a lot less, and in fact, the cost is determined at the time of an option grant, which is aligned with the Fair Market Value of the business, also known as the 409A valuation. It is very common to see the 409A at 25-50% of the preferred price that investors pay. The gap between the 409A price and the preferred price typically converges as a company gets closer to IPO, and after the IPO, they will be the same.

So let’s say you’re an employee who joined the company after that $30M fundraising round that valued the company at $200M. The investors paid $20/share for their stock, but as an employee buying common stock by exercising your ISOs, you might be paying something closer to $5/share, which would actually imply a $50M fair market value for the business. As long as the price that you get paid out clears that $50M number, you haven’t lost anything, although your payout won’t be quite as golden as you might have expected.

This all comes back to this initial discussion of multiple compression. Even though multiples are going down, the valuation that you, as an employee, needs the company to get to in order to make money (where, admittedly, make money is defined as anything more than $0, though most people probably would not be super excited to have funded an Applebee’s trip with their lottery ticket) is likely way lower than you expect.

So the real question to ask is: what valuation do you have to clear in order for your options to break even (i.e. you can sell them for exactly what you buy them for), and how likely is it that your company will clear that hurdle? And how likely is it that your company will clear that hurdle significantly enough to produce an exit that is meaningful to you? I’ll leave that as an exercise for the reader.

Very timely article - Thanks for writing. Snowflakes journey from 200x to 28x in 2 years. However, in long run the revenue growth decides how much returns we get as investors - snowflake is growing very fast. I have some charts but can't post here.